Blockchain technology's decentralized nature is revolutionizing cybersecurity in several key ways: 1. Distributed Ledger: Blockchain operates as a distributed ledger, meaning that data is stored across a network of computers (nodes) rather than a single central server. This makes it much moreRead more

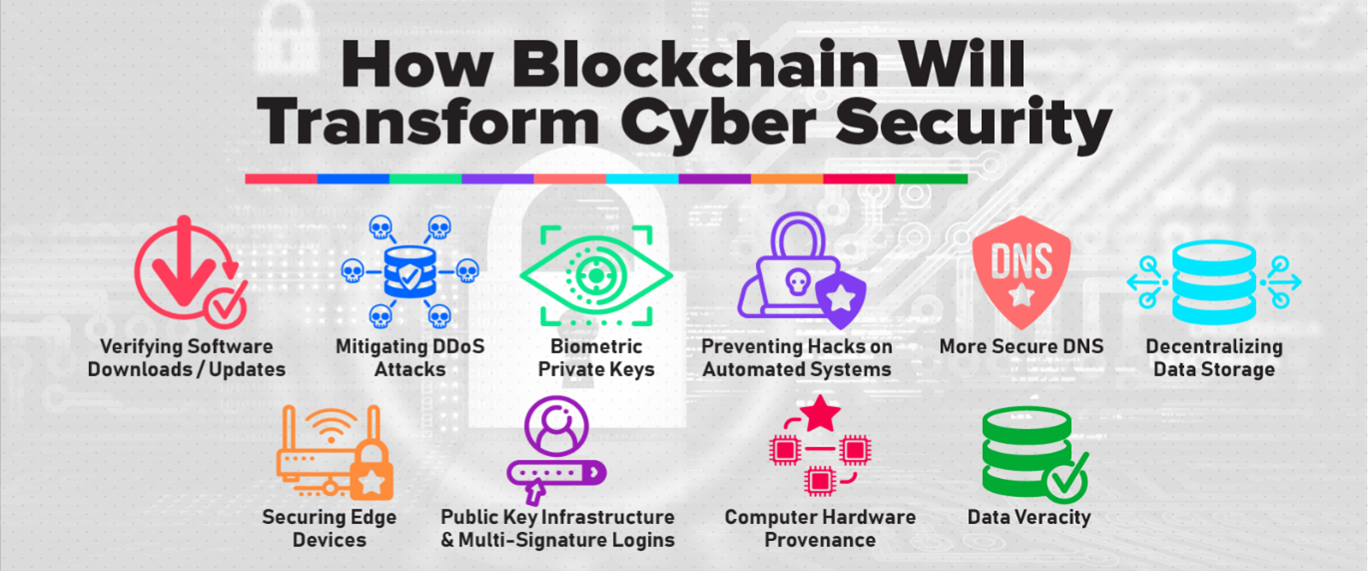

Blockchain technology’s decentralized nature is revolutionizing cybersecurity in several key ways:

1. Distributed Ledger: Blockchain operates as a distributed ledger, meaning that data is stored across a network of computers (nodes) rather than a single central server. This makes it much more difficult for hackers to attack because there is no single point of failure. Compromising the network would require simultaneously attacking a majority of the nodes.

2. Immutability: Once data is recorded on a blockchain, it is extremely difficult to alter. This immutability helps prevent unauthorized changes and tampering. Each block is cryptographically linked to the previous one, creating a secure chain of information.

3. Transparency and Traceability: Transactions on a blockchain are transparent and can be traced back to their origin. This transparency deters fraudulent activities and enhances trust, as all participants can see the same information and verify it independently.

4. Decentralized Consensus: Blockchain uses consensus mechanisms (such as Proof of Work or Proof of Stake) to validate transactions. This means that no single entity controls the verification process, reducing the risk of corruption or manipulation.

5. Enhanced Security Protocols: Blockchain technology employs advanced cryptographic techniques to secure data. Public and private keys, along with digital signatures, ensure that only authorized users can access and execute transactions.

6. Smart Contracts: These are self-executing contracts with the terms directly written into code. They automatically enforce and execute agreements when predetermined conditions are met, reducing the need for intermediaries and enhancing security through automation.

By decentralizing data storage and verification, blockchain technology significantly enhances cybersecurity, making systems more resilient to attacks, reducing fraud, and increasing trust among users.

See less

Cryptocurrency refers to digital or virtual currencies that use cryptography for security and operate independently of a central authority, such as a government or financial institution. Bitcoin is the most well-known example, but there are thousands of other cryptocurrencies with various features aRead more

Cryptocurrency refers to digital or virtual currencies that use cryptography for security and operate independently of a central authority, such as a government or financial institution. Bitcoin is the most well-known example, but there are thousands of other cryptocurrencies with various features and purposes.

### Benefits of Cryptocurrency:

1. **Decentralization**: Cryptocurrencies operate on decentralized networks using blockchain technology, which means they are not controlled by any single entity. This can potentially reduce the risk of fraud or manipulation.

2. **Security**: Cryptography ensures the security of transactions and control of new coin creation. Blockchain’s immutable nature makes transactions transparent and resistant to alteration.

3. **Accessibility**: Cryptocurrencies can be accessed by anyone with an internet connection, providing financial services to populations without access to traditional banking systems.

4. **Lower Transaction Fees**: Transactions conducted with cryptocurrencies can have lower fees compared to traditional financial systems, especially for international transfers.

5. **Innovation**: Cryptocurrencies have spurred technological innovation in finance and beyond, such as smart contracts and decentralized applications (DApps).

### Challenges of Cryptocurrency:

1. **Volatility**: Cryptocurrency prices can be highly volatile, making them risky as investments and less predictable as a medium of exchange.

2. **Regulatory Uncertainty**: Many governments are still developing regulations for cryptocurrencies, which can lead to uncertainty for users and businesses.

3. **Security Concerns**: While blockchain itself is secure, cryptocurrency exchanges and wallets have been targeted by hackers, leading to significant losses.

4. **Scalability**: Some cryptocurrencies face challenges in scaling to handle large numbers of transactions quickly and efficiently.

5. **Adoption and Usability**: Cryptocurrencies still face barriers to mainstream adoption, such as user interface complexity and limited merchant acceptance.

### Conclusion:

Cryptocurrencies offer potential benefits like decentralization, security, and accessibility, but they also come with challenges such as volatility, regulatory uncertainty, and security risks. Their future adoption and impact will depend on how these challenges are addressed and whether they can overcome barriers to become widely accepted in mainstream finance and commerce.

See less