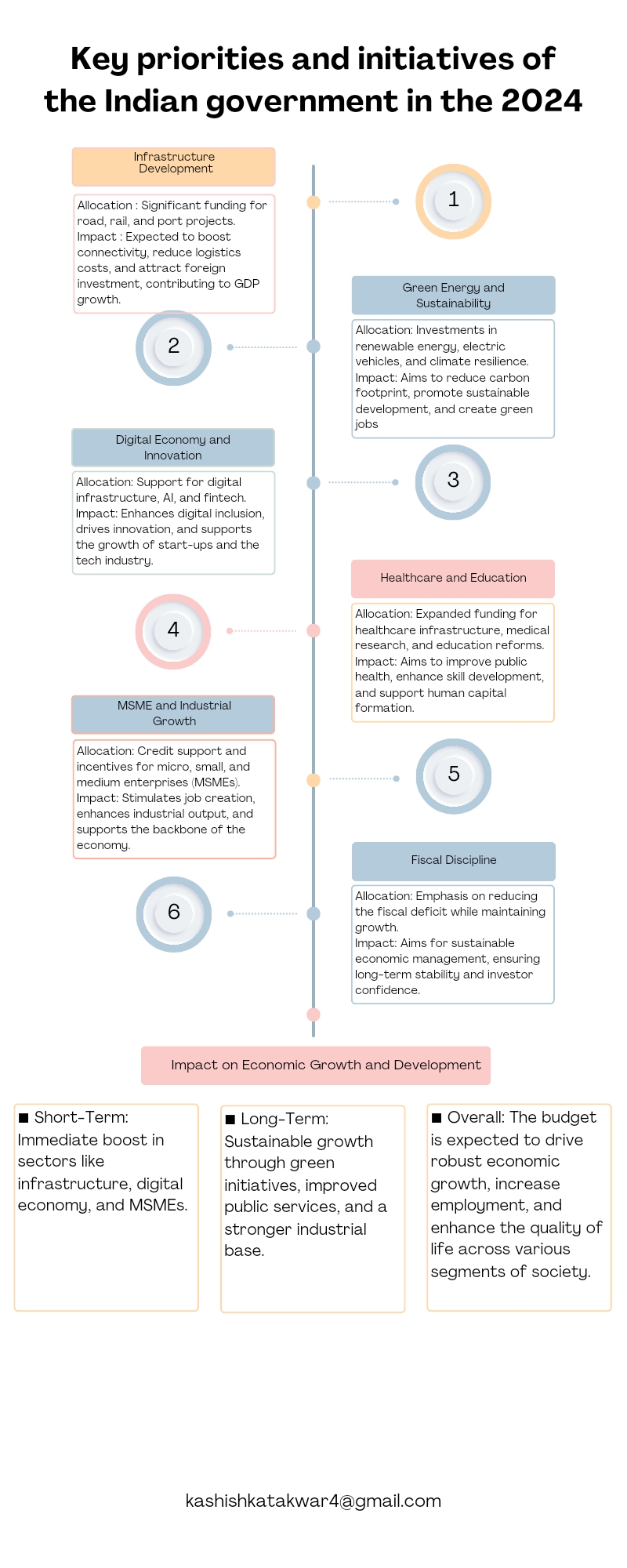

Background and context of GST (Goods and Services Tax) in India- introduction and adoption Effect on administrative efficiency – unified tax structure, decreasing cascading effect Impact on revenue collection- positive or negative Challenges in administration of GST Future prospects and recommendations

The judicial system in India underwent significant development under British rule. The British established a hierarchical court structure with the Supreme Court at the apex followed by High Courts, District Courts and lower courts. This structure remains largely intact today. Key reforms and their iRead more

The judicial system in India underwent significant development under British rule. The British established a hierarchical court structure with the Supreme Court at the apex followed by High Courts, District Courts and lower courts. This structure remains largely intact today.

Key reforms and their impact –

- Charter Act of 1726 established the first Supreme Court in India marking the beginning of a modern judicial system.

- Regulating Act of 1773 introduced the concept of a hierarchical court structure and established the Calcutta High Court.

- Indian High Courts Act of 1861 established High Courts in Bombay, Madras and Calcutta introduced the concept of appellate jurisdiction.

- Code of Civil Procedure 1859 standardized civil procedure across India.

- Indian Evidence Act 1872 codified the law of evidence, ensuring consistency in judicial proceedings.

The evolution of courts and legal frameworks during the colonial period shaped the current judicial structure of India in several ways –

- The British established court hierarchy remains in place today.

- The British introduced codified laws such as the Indian Penal Code and the Code of Civil Procedure which continue to govern Indian law.

- The British established an independent judiciary which has been maintained in post colonial India.

These reforms and the overall development of the judicial system under British rule have had a lasting impact on the Indian judiciary shaping its structure, laws and procedures.

See less

GST in India: Overview and Impact The Goods and Services Tax (GST), launched on the first of July 2017 is one composite tax that has replaced several indirect taxes. The major aim of implementing the GST of the central government is to minimize the tax on tax or ‘The Tax on Tax’ concept and have cenRead more

GST in India: Overview and Impact

The Goods and Services Tax (GST), launched on the first of July 2017 is one composite tax that has replaced several indirect taxes. The major aim of implementing the GST of the central government is to minimize the tax on tax or ‘The Tax on Tax’ concept and have centralisation of taxation system that means ‘One Nation, One Tax’.

Administrative Efficiency

GST improved the administrativeness by consolidating different taxes into one architecture. The GST Network services through which businessmen and women can register themselves online and file their tax returns, has made compliances simple and reduced the problem of bureaucratic red-tapism. Taking this into more details, the government of India has introduced a new mechanism known as e-way bill mechanism that has eased the movement of good across states.

The mechanism of input tax credit removed the problem of the cascading nature of taxes and alleviated the effective tax rate borne by businesses and also enhanced compliance.

The effect on sustainable revenue streams has been positive. GST improved the growth of the unorganized sector by including them into the tax regime to eliminate tax evasion through the application of technology. Still, at first, states faced a decline in their revenues, but such a deficit was covered by the central authorities.

The following is an analysis of some of the challenges that erupt when implementing GST.

Although improvements have been made, GST still faces many problems:

1. Complex Compliance: The dynamic environment and the complex and multiple tax slabs add to the confusion.

2. Technological Gaffes: There are times that GST portal provides and displays errors when traffic is heavily congested.

3. Delayed Refund: The exporting businesses experience long delays with regard to their refund.

4. Tax Avoidance: frauds and other bogus bills

Future Future Prospects and Recommendations

– Simplify compliance issue by decreasing the GST Rates.

B) Enhance the Capacity of GSTN in order to deal a sheer traffic of business.

Enhancing Anti-Evasion Mechanisms with the support of data analytical processing.

Investment was made on the Efficiency aspect of the Refund mechanism in order to help business

Conclusion

GST is been one of the most revolutionary changes in the taxation structure of India improving the efficiency of revenue collection. Nonetheless, its effectiveness can be optimised by addressing compliance concerns, and technology improvements, as well as improved center-state policies in goodness.

See less